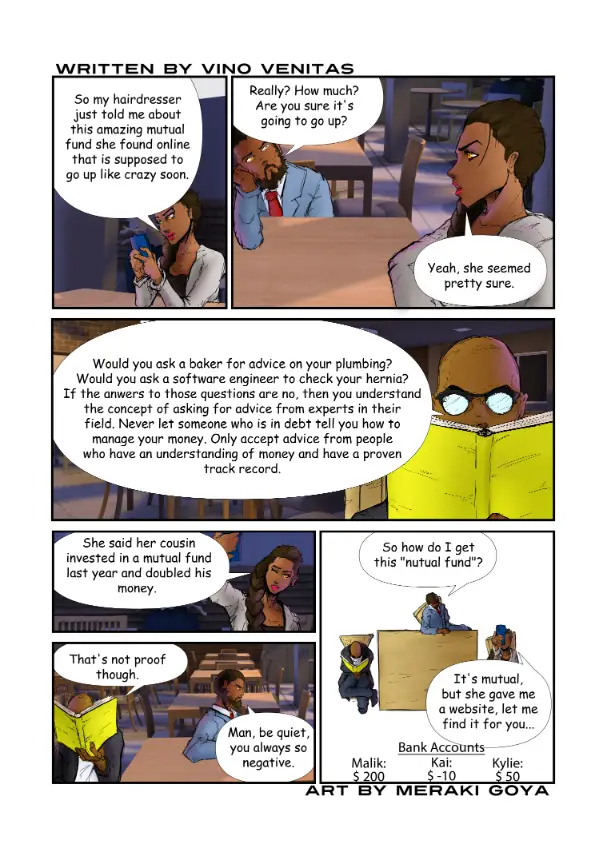

Mastering Personal Finances: “A Part of All I Earn is Mine to Keep”

In the realm of personal finance, there’s a timeless principle that has stood the test of time: “A part of all I earn is mine to keep.” This powerful statement, originally coined by George S. Clason in his book “The Richest Man in Babylon,” encapsulates the essence of wealth-building and financial stability. Let’s delve into what this principle means and how it can shape your journey toward financial independence.

Understanding the Principle

At its core, “A part of all I earn is mine to keep” emphasizes the importance of saving and investing a portion of your income before allocating it to expenses. It advocates for a mindset shift where saving becomes a priority rather than an afterthought. Instead of spending all that you earn, this principle encourages you to set aside a portion of your income for yourself—your future self.

Pay Yourself First

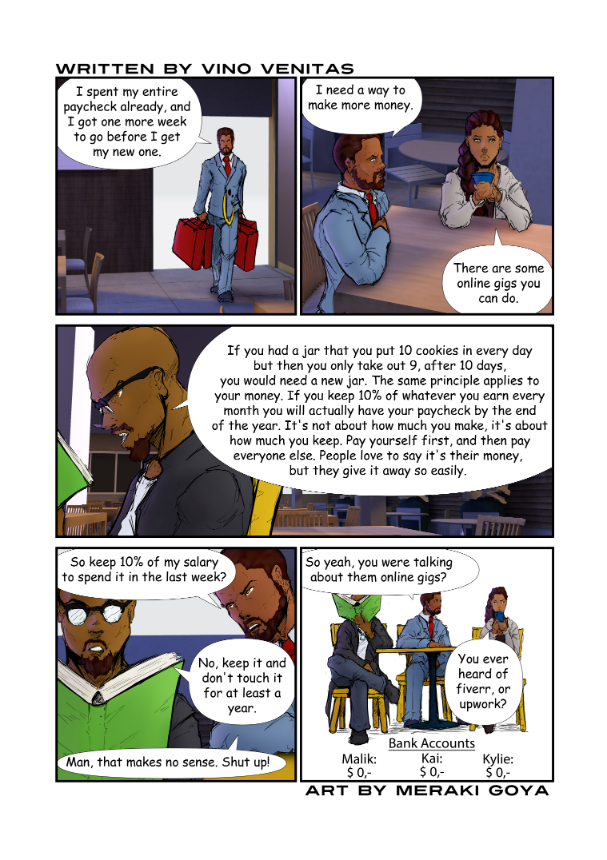

The concept of “paying yourself first” aligns closely with this principle. Rather than waiting until the end of the month to see if there’s anything left to save, treat your savings as a non-negotiable expense. Set up automatic transfers from your paycheck to your savings or investment accounts before allocating funds to other expenses. By prioritizing saving, you ensure that you consistently build wealth over time.

Building Financial Security

By adhering to the principle of keeping a part of all you earn, you lay the foundation for financial security. Emergency funds, retirement savings, and investments are all essential components of a robust financial plan. By consistently saving a portion of your income, you create a safety net that protects you from unexpected expenses and allows you to pursue your long-term financial goals.

The Power of Compound Interest

One of the most compelling reasons to adopt this principle is the power of compound interest. When you consistently save and invest a portion of your income, your money has the opportunity to grow over time. Reinvesting dividends and allowing your investments to compound can significantly accelerate wealth accumulation. The earlier you start saving, the more time your money has to grow, emphasizing the importance of taking action now.

Practical Steps to Implement the Principle

- Set Clear Savings Goals: Define your financial objectives, whether it’s building an emergency fund, saving for a down payment, or funding your retirement.

- Automate Your Savings: Take advantage of technology to automate your savings process. Set up automatic transfers from your checking account to your savings or investment accounts.

- Track Your Expenses: Monitor your spending habits to identify areas where you can cut back and allocate more towards savings.

- Review and Adjust Regularly: Periodically review your savings and investment strategy to ensure it aligns with your goals and adjust as necessary.

Conclusion

In a world where consumerism often encourages us to spend beyond our means, embracing the principle of “A part of all I earn is mine to keep” is a powerful antidote. By prioritizing saving and investing, you take control of your financial future and pave the way for long-term prosperity. Start small, but start today. Remember, every dollar saved and invested is a step closer to achieving your financial dreams.